J.P. Morgan Asset Management - Investing in Smaller Companies

It’s a relatively well understood concept that buying small and mid-sized company shares can bring more attractive returns for investors willing to take the price of higher risk. What most UK investors don’t fully appreciate is the astonishingly large difference in returns between the performance of small and mid-cap shares and mega-cap shares over the very long-term.

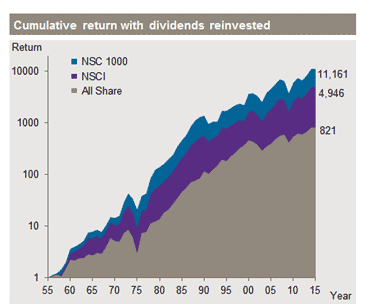

Data compiled by stockbrokers Numis Securities paints this in stark relief. In the last 60 years, the smallest 2% of UK equities produced a cumulative total return of 11,160%, with dividends reinvested. Over the same time period, the smallest 10% of the UK equity market produced a cumulative total return of 4,946%. By comparison, the FTSE All Share over that same 60 years would have netted just 821% cumulative returns, with dividends reinvested (Source: Numis Securities, as at 31 December 2015).

Small and mid-cap equities are more representative of UK Plc, with significantly greater exposure to the domestic economy than large-caps. For example, whilst the UK represents only around a quarter of FTSE100 revenues, it represents over half of the revenue generated by the FTSE250.

These companies may also have the intrinsic advantage of where they sit in the business life cycle. Often they are younger companies, earlier in their evolution, with significantly more potential to achieve super normal growth, which ultimately generates superior equity returns. If we can identify those companies early in their life span, we can hold that investment all the way through their maturation into larger companies. As compared to their larger brethren, small and mid-cap business growth by definition can be a much higher percentage of their starting point. It is worth noting that some of these companies, particularly mid-caps, can be market leaders in their particular niche, thereby delivering the competitive advantages enjoyed by traditional large-cap companies, but with the potential for delivering that higher growth.

Source: Numis/ Paul Marsh and Elroy Dimson - London Business School. Total return index, Log scale. NSCI = Numis Smaller Companies Index. The NSCI 1000 covers the bottom two percent of the UK equity market by value (ex Investment Trusts), The NSCI covers the bottom ten percent of the UK equity market. Data to 31 December 2015. Past performance is not an indication of future performance.

In terms of the outlook for continued outperformance, we expect to continue to see small and mid-caps thrive, thanks in part to their end market exposure. As more small and mid-caps are domestically oriented, theyve benefited from the strong UK economy recovery, which is currently outpacing much of the rest of the world. In addition, the industry sectors are more diversified than the large caps, which are more dominated by natural resources. This less concentrated exposure and the more broadly balanced mix of businesses make this sector look attractive.

Author

Simon Crinage

Head of Investment Trusts, J.P. Morgan Asset ManagementFebruary 2016

Please note that these are the views of Simon Crinage, Head of Investment Trusts, J.P. Morgan Asset Management and should not be interpreted as the views of RL360.