Schroders - What does a landslide Labour UK election win mean for the economy and markets?

A secure majority government should reduce political instability for the nation, helping companies and investors to anticipate policy.

Azad Zangana, Senior European Economist and Strategist:

'The UK is going through its biggest political change since Brexit, as the general election results suggest that the Labour Party has won a landslide mandate to govern.

‘Labour’s majority is on a scale with the one achieved by Tony Blair in his historic 1997 landslide victory, although Blair won on a much larger share of the vote. Moreover, the change in votes and seats compared to the 2019 election means that this is one of the largest political swings in the UK’s history.

‘The election results show that the surge in support for the right-wing Reform UK party severely hurt the outgoing Conservative government, where Reform frequently beat the Conservatives into second place in a number of constituencies. Often, where the votes of the two parties are combined, they would have beaten Labour to those seats.

‘However, the results shows that the Conservatives have lost over two-thirds of their seats, leading to major questions over the future of the party.

‘Keir Starmer will become the first Labour prime minister since May 2010, and will have to quickly get to work to form his government, before heading off to an important NATO summit next week.'

Investors and businesses benefit from political stability

‘In terms of policy changes, the election campaign revealed very little new information about the Labour government’s plans. Its stated priority is to grow the economy and provide security and stability, the importance of which should not be overlooked from the perspective of investors.

‘The last parliament has been dogged by political instability and uncertainty. Since the December 2019 election, there have been three prime ministers and five chancellors.

‘A recent study by Strong and Stable found that the average cabinet minister’s tenure fell to just eight months – the lowest average over the 1974-2023 period. Although governed by the same Conservative Party, this level of instability makes it very difficult for companies and investors to anticipate policy changes and work with government.

‘Having had a largely stagnant economy since outgoing Prime Minister Rishi Sunak took office, the focus on boosting growth to enable greater spending on public services is a logical approach to the Labour Party’s objective.

‘In the near-term, the economy is set to rebound following a recession at the end of last year, but structural challenges remain including an aging population and strained trade relationships. Reforming the planning system and making the UK a more attractive destination for foreign direct investment should be top of the government’s priorities.

‘The likely new chancellor Rachel Reeves plans to exclude public investment from the government’s self-imposed borrowing rules. This is a signal that Labour plans to borrow more to invest.

‘The lines between public current spending and investment have in the past been blurred, which may in time raise some concerns.'

Tough legacy to inherit given heavy existing tax burden

‘Moreover, there is a general expectation that some taxes will have to rise in due course, despite Labour’s manifesto pledge to freeze most personal taxes. This will be difficult given the “fiscal drag” which is occurring as the result of frozen income tax thresholds for the past seven years.

‘With more and more workers paying higher marginal rates, the nation’s tax burden is expected to rise to its highest level since 1948 by the end of the Office for Budget Responsiblity’s current forecast period – a tough legacy to inherit.

‘Overall, the change in government, particularly with such a large majority, should reduce political instability for the nation. A change in the direction of policy back to growing public services is likely to lead to looser fiscal policy and boost economic growth.

‘However, the significant support for Reform UK is likely to put pressure on Labour to restrict inward migration. This would limit the economy’s growth prospects as its aging population is already impacting staff availability, pushing wage inflation higher.

‘Given the result was largely as expected, there has been little to no reaction from markets. Members of the Monetary Policy Committee (MPC) at the Bank of England (BoE) have not been allowed to give speeches in recent weeks owing to election purdah rules.

‘They are, however, expected to return to public speaking soon, and again start to signal imminent cuts to interest rates, potentially from August onwards.’

What does the result mean for UK capital market reforms?

Richard Fox, Head of Public Policy, UK:

‘While politically seismic – from a policy point of view, at least for financial services, we largely expect continuity under the new government. In opposition Labour supported the main building blocks of the previous administration’s reform agenda, including important packages like the Edinburgh Reforms and Mansion House.

‘We expect these to continue broadly as they are. Key themes like UK competitiveness, green finance and fintech and innovation will remain front and centre. But there are some important things to look out for. Labour has committed to a broad review of the full suite of UK pensions issues, and how the new government sets up their proposed “National Wealth Fund” will also be one to watch.’

What are the implications for equity markets?

Sue Noffke, Head of UK Equities:

‘An October Budget will be the first test for the market to assess Labour on its fiscal policies with a spending review, but for now sterling is steady, as are gilts. The mini-Budget blowout in 2022 showed how poor economic management can negatively impact investor confidence and UK assets.

‘It seems bizarre to say this, but it’s probably helpful that we had that blowout, and I think the market knows this too. It has shown everyone what’s not possible and the chancellor-in-waiting Rachel Reeves seems to have really taken the lessons on board.

‘There is still some concern among business that taxes will rise if there’s a shock or growth doesn’t come through. It’s not being talked about today, but it could come in due course.’

‘The business community seems relaxed about the prospect of a Labour government. While there has been concern about the reality of an inexperienced administration with a lot of new MPs, behind the scenes, there’s been a lot of coaching and consultation with business leaders, which is reassuring.'

What a “1997 moment” might mean for UK equities

‘One of the most notable comments I’ve heard was from a seasoned UK executive who has led several FTSE 100 companies. Far from being concerned about the prospect of a Labour government, he suggested that this could be a 1997 moment that brings some real excitement about the UK. “Things can only get better,” he told me, referring to the D:Ream song famously played after Tony Blair’s 1997 election victory.

‘With regards to UK equities, there’s so much that is oven ready in terms of capital market reform which could benefit them, such as making it easier to float and undertake M&A (mergers and acquisitions). There’s real momentum behind these initiatives (see comment from Richard Fox, above).

‘In the immediate term Labour inherit an economy with some positive momentum, inflation has eased such that interest rate cuts are on the cards for the second half of 2024. Rate cuts would provide a potential boost to real incomes for households and domestically focussed areas of the equity market.

‘In terms of potentially market moving policy changes which may not yet be discounted, we expect to see a reversal of the ban on onshore windfarms, and a reform of the planning system. Changes in these areas would have direct implications for UK quoted utility and associated support service and construction companies – another potential boost to UK domestics (see comment from Graham Ashby, below).

‘Such changes could open up great investment opportunities for companies involved in providing grid infrastructure for the renewable transition, while many quoted housebuilders should benefit from planning reform.

‘It’s interesting to see housebuilders performing very strongly on the back of the election result, in line with the more domestically focussed mid-sized companies generally.’

Graham Ashby, Fund Manager, UK All Cap:

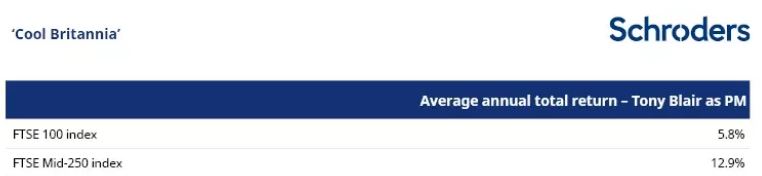

‘The Labour Party recently highlighted that the UK equity market typically performs better when it is in power. We’ve had a look at the data, and it’s interesting to see that mid-sized companies in the FTSE Mid-250 index significantly outperformed larger-sized companies in the FTSE 100 index during Tony Blair’s tenure as Prime Minister.' (see table, below)

Source: Schroders/Bloomberg, 2 May 1997 to 27 June 2007, 612837

‘This compares to the more recent experience of mid-sized companies suffering a topsy-turvy decade of underperformance. Higher risk assets, such as mid-sized companies, should in theory deliver higher returns, but several years of investment outflows from UK mid- and small-sized companies seem to have disrupted the usual risk/return trade-off.

‘Drawn in by the boom in US technology stocks, retail investors have cut exposure to actively managed UK funds which focus on investing in mid- and small-sized companies. At the same time, domestic pension funds have reduced allocations to volatile equities to better manage their liabilities. It’s difficult not to conclude mid- and small-sized companies have been denied the required capital to achieve their full growth potential.

‘What’s to stop the new government from mandating a certain minimum exposure for pension funds, following on from the previous administration's announcement of a British ISA? UK pension fund allocations to domestic equities are, after all, unusually low versus other jurisdictions.

‘Economic and market conditions may be very different to 1997 when Tony Blair began his 10-year term in office, and the Labour Party has a historical reputation as being rather pro-union and anti-business. That said, a new Labour government may have important positive implications for UK capital markets and equities.’

What are the implications for fixed income markets?

James Ringer, Fixed Income Portfolio Manager:

‘We’re not seeing any significant moves in gilts or UK corporate bonds in the wake of the election result, but that’s not surprising since a Labour victory of roughly this magnitude has been the likely outcome since the election was called. The incoming administration has been keen to stress a commitment to fiscal restraint, which has reassured markets.

‘But there remains a sense that, once in government, Labour’s cautious fiscal approach will need to adjust to the reality of additional public spending needs, meaning potentially higher levels of borrowing longer-term. The widely-held expectation is that a Labour government will provide a more stable business environment and - over the medium term - better relations with the EU.

‘This kind of backdrop should be broadly positive for UK corporate bonds, and should also be supportive for sterling: again, this already seems to be reflected in market pricing, with sterling strengthening slightly versus the euro and the US dollar over the last few weeks.

‘In practice, the more immediate consideration for markets is that the BoE is back in the driving seat, having been under a self-imposed communications blackout since 23 May (another reason why gilt yields have not moved much in recent weeks). Comments from MPC members due over the next few days will help give a clearer view on the likelihood of an August rate cut. In the near term, shifting monetary policy expectations will have a much greater impact on gilt pricing than any fiscal policy speculation.’

Important Information

This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

July 2024

Please note that these are the views of Schroders and should not be interpreted as the views of RL360.